Fixed assets are first recorded as assets that later are gradually “expensed off,” or claimed as a business expense, over time. If adjusting entries are not prepared, some income, expense, asset, and liability accounts may not reflect their true values when reported in the financial statements. Adjusting entries affect financial statements by ensuring that they accurately reflect a company’s financial position. This can have serious consequences for a company’s financial health and reputation.

The Process of Recording Adjustment Entries

The revenue recognition principle requires businesses to recognize revenue when it is earned, regardless of when payment is received. Adjustment entries are necessary to ensure that revenue is recognized in the correct period, even if payment has not been received. Adjustment entries are usually made in the general journal, which is used to record transactions that do not fit into any of the other journals. Each entry consists of a debit and a credit, and is recorded in accordance with the double-entry accounting system.

Depreciation Expense

Here are the Prepaid Taxes and Taxes Expense ledgers AFTER the adjusting entry has been posted. Here are the Prepaid Rent and Rent Expense ledgers AFTER the adjusting entry has been posted. Here are the ledgers that relate to the purchase of prepaid rent when the transaction above is posted. Here are the Prepaid Insurance and Insurance Expense ledgers AFTER the adjusting entry has been posted. Here are the ledgers that relate to the purchase of prepaid insurance when the transaction above is posted. These are the five adjusting entries for deferred expenses we will cover.

Create a Free Account and Ask Any Financial Question

Adjusting entries, also called adjusting journal entries, are journal entries made at the end of a period to correct accounts before the financial statements are prepared. Adjusting entries are most commonly used in accordance with the matching principle to match revenue and expenses in the period in which they occur. Income statement accounts that may need to be adjusted include interest expense, insurance expense, depreciation expense, and revenue. The entries are made in accordance with the matching principle to match expenses to the related revenue in the same accounting period. The adjustments made in journal entries are carried over to the general ledger that flows through to the financial statements.

Mistake: Incorrect Accounting Entries

- To illustrate let’s assume that on December 1, 2023 the company paid its insurance agent $2,400 for insurance protection during the period of December 1, 2023 through May 31, 2024.

- If you do your own accounting, and you use the accrual system of accounting, you’ll need to make your own adjusting entries.

- Accrued expenses are expenses made but that the business hasn’t paid for yet, such as salaries or interest expense.

- That skews your actual expenses because the work was contracted and completed in February.

An adjusting journal entry involves an income statement account (revenue or expense) along with a balance sheet account (asset or liability). It typically relates to the balance sheet accounts for accumulated depreciation, allowance for doubtful accounts, accrued expenses, accrued income, prepaid expenses, deferred revenue, and unearned revenue. When doing your accounting journal entries, you are tracking how money moves in your business. Adjusting entries are the changes you make to these journal entries you’ve already made at the end of the accounting period. You can adjust your income and expenses to more accurately reflect your financial situation.

The word “expense” implies that the taxes will expire, or be used up, within the month. An expense is a cost of doing business, and it cost $100 in business license taxes this month to run the business. There are two ways this information can be worded, both resulting in the same adjusting entry above. The word “expense” implies that the rent will expire, or be used up, within the month.

For example, going back to the example above, say your customer called after getting the bill and asked for a 5% discount. If you granted the discount, you could post an adjusting journal entry to reduce accounts receivable and revenue by $250 (5% of $5,000). Adjusting entries are changes to journal entries you’ve already recorded.

To transfer what expired, Taxes Expense was debited for the amount used and Prepaid Taxes was credited to reduce the asset by the same amount. Any remaining balance in the Prepaid Taxes account is what you have left to use in the future; it continues to be an asset since it is still available. At the end of the month 1/12 of the prepaid taxes will be used up, and you must account for what has expired.

Adjustment entries are necessary to ensure that all revenue and expenses are recorded in the correct period, even if payment has not been made or received. Deferrals are revenues or expenses that have been paid or received in advance. To record a deferral, an accountant would debit an asset account and credit a revenue or expense account.

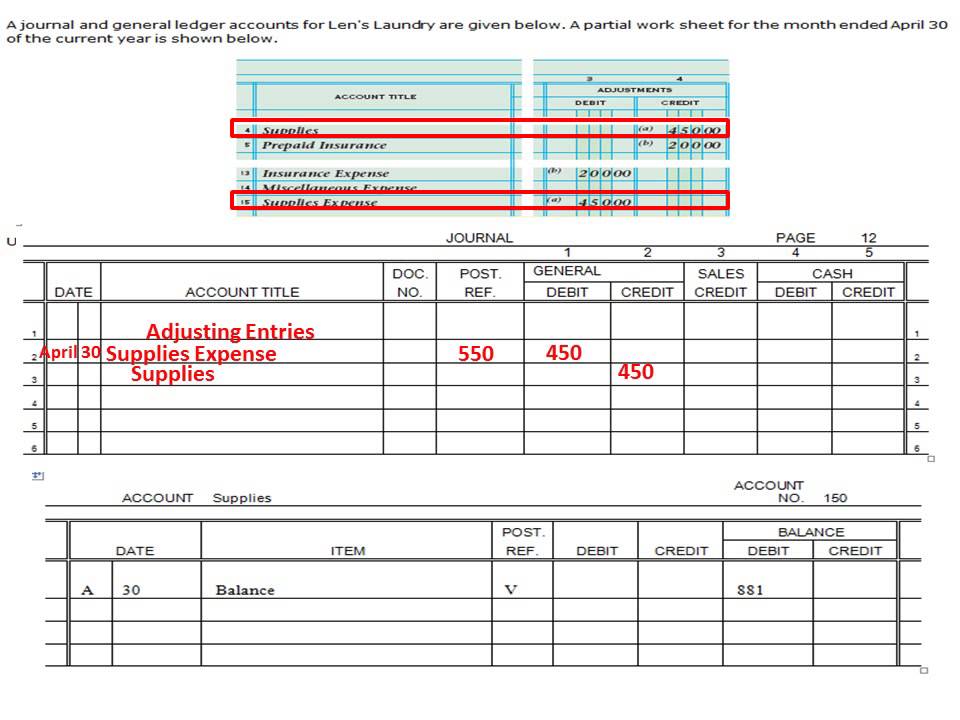

An expense is a cost of doing business, and it cost $1,000 in rent this month to run the business. The word “expense” implies that the insurance will expire, or be used up, within the month. An expense is a cost of doing business, and restaurant and food service supply chain solutions it cost $100 in insurance this month to run the business. The word “expense” implies that the supplies will be used within the month. An expense is a cost of doing business, and it cost $100 in supplies this month to run the business.

The two examples of adjusting entries have focused on expenses, but adjusting entries also involve revenues. This will be discussed later when we prepare adjusting journal entries. Making adjusting entries is a way to stick to the matching principle—a principle in accounting that says expenses should be recorded in the same accounting period as revenue related to that expense. You had purchased supplies during the month and initially recorded them as an asset because they would last for more than one month. By the end of the month you used up some of these supplies, so you reduced the value of this asset to reflect what you actually had on hand at the end of the month ($900).