Fees earned from providing services and the amounts of merchandise sold. Under the accrual basis of accounting, revenues are recorded at the time of delivering the service or the merchandise, even if cash is not received at the time of delivery. After 60 months, the balance in the Accumulated Depreciation account is $6,000 and therefore the equipment is fully depreciated and has no value.

Depreciation Expense

Another situation requiring an adjusting journal entry arises when an amount has already been recorded in the company’s accounting records, but the amount is for more than the current accounting period. To illustrate let’s assume that on December 1, 2023 the company paid its insurance agent $2,400 for insurance protection during the period of December 1, 2023 through May 31, 2024. The $2,400 transaction was recorded in the accounting records on December 1, but the amount represents six months of coverage and expense.

Common Examples of Adjustment Entries

“Deferred” means “postponed into the future.” In this case you have purchased something in “bulk” that will last you longer than one month, such as supplies, insurance, rent, or equipment. Rather than recording the item as an expense when you purchase it, you record it as an asset (something of value to the business) since you will not use it all up within a month. At the end of the month, you make an adjusting entry for the part that you did use up—this is an expense, and you debit the appropriate expense account. The credit part of the adjusting entry is the asset account, whose value is reduced by the amount used up. Any remaining balance in the asset account is what you still have left to use up into the future.

- The word “expense” implies that the taxes will expire, or be used up, within the month.

- Any remaining balance in the asset account is what you still have left to use up into the future.

- That’s why most companies use cloud accounting software to streamline their adjusting entries and other financial transactions.

What is an adjusting entry?

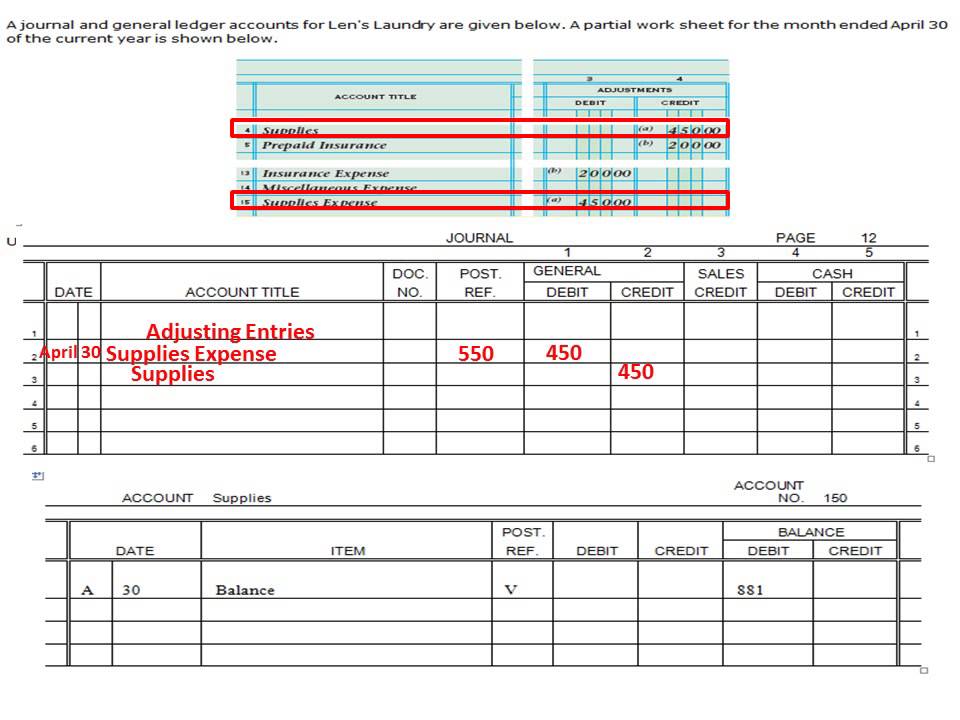

Here is an example of the Prepaid Insurance account balance at the end of October. The $100 balance in the Supplies Expense account will appear on the income statement at the end of the month. The remaining $900 in the Supplies account will appear on the balance sheet. This amount is still an asset to the company since it has not been used yet.

These entries can also involve the use of supplies accounts to record the use of inventory or other supplies. Estimating too high or too low can tax calculator return and refund estimator 2020 also lead to incorrect financial statements. This can happen when estimates are not updated or when they are based on incorrect assumptions.

Your Revenue Reporting May Be Inaccurate

The main purpose of adjusting entries is to update the accounts to conform with the accrual concept. At the end of the accounting period, some income and expenses may have not been recorded or updated; hence, there is a need to adjust the account balances. The four types of adjustments in accounting include accruals, deferrals, reclassifications, and estimates. Accruals and deferrals involve adjusting entries to record transactions that have occurred but have not yet been recorded. Reclassifications involve moving amounts between accounts, while estimates involve adjusting amounts based on expected future events. The accrual basis of accounting recognizes revenue and expenses when they are earned or incurred, regardless of when payment is received or made.

In August, you record that money in accounts receivable—as income you’re expecting to receive. Then, in September, you record the money as cash deposited in your bank account. The most common method used to adjust non-cash expenses in business is depreciation. In other words, we are dividing income and expenses into the amounts that were used in the current period and deferring the amounts that are going to be used in future periods. In this article, we shall first discuss the purpose of adjusting entries and then explain the method of their preparation with the help of some examples.

An adjusting entry is needed so that December’s interest expense is included on December’s income statement and the interest due as of December 31 is included on the December 31 balance sheet. The adjusting entry will debit Interest Expense and credit Interest Payable for the amount of interest from December 1 to December 31. When you make an adjusting entry, you’re making sure the activities of your business are recorded accurately in time.

Sometimes companies collect cash from their customers for goods or services that are to be delivered in some future period. Such receipt of cash is recorded by debiting the cash account and crediting a liability account known as unearned revenue. At the end of the accounting period, the unearned revenue is converted into earned revenue by making an adjusting entry for the value of goods or services provided during the period. Adjustment entries are accounting entries made at the end of an accounting period to record transactions that have occurred but have not yet been recorded. These entries are necessary to ensure that financial statements accurately reflect the company’s financial position and performance.

You will also learn the second trial balance prepared in the accounting cycle – the adjusted trial balance. It is normal to make entries in the accounting records on a cash basis (i.e., revenues and expenses actually received and paid). If you use accounting software, you’ll also need to make your own adjusting entries.

This is usually done with large purchases, like equipment, vehicles, or buildings. Once you’ve wrapped your head around accrued revenue, accrued expense adjustments are fairly straightforward. They account for expenses you generated in one period, but paid for later. With the Deskera platform, your entire double-entry bookkeeping (including adjusting entries) can be automated in just a few clicks.

Comments